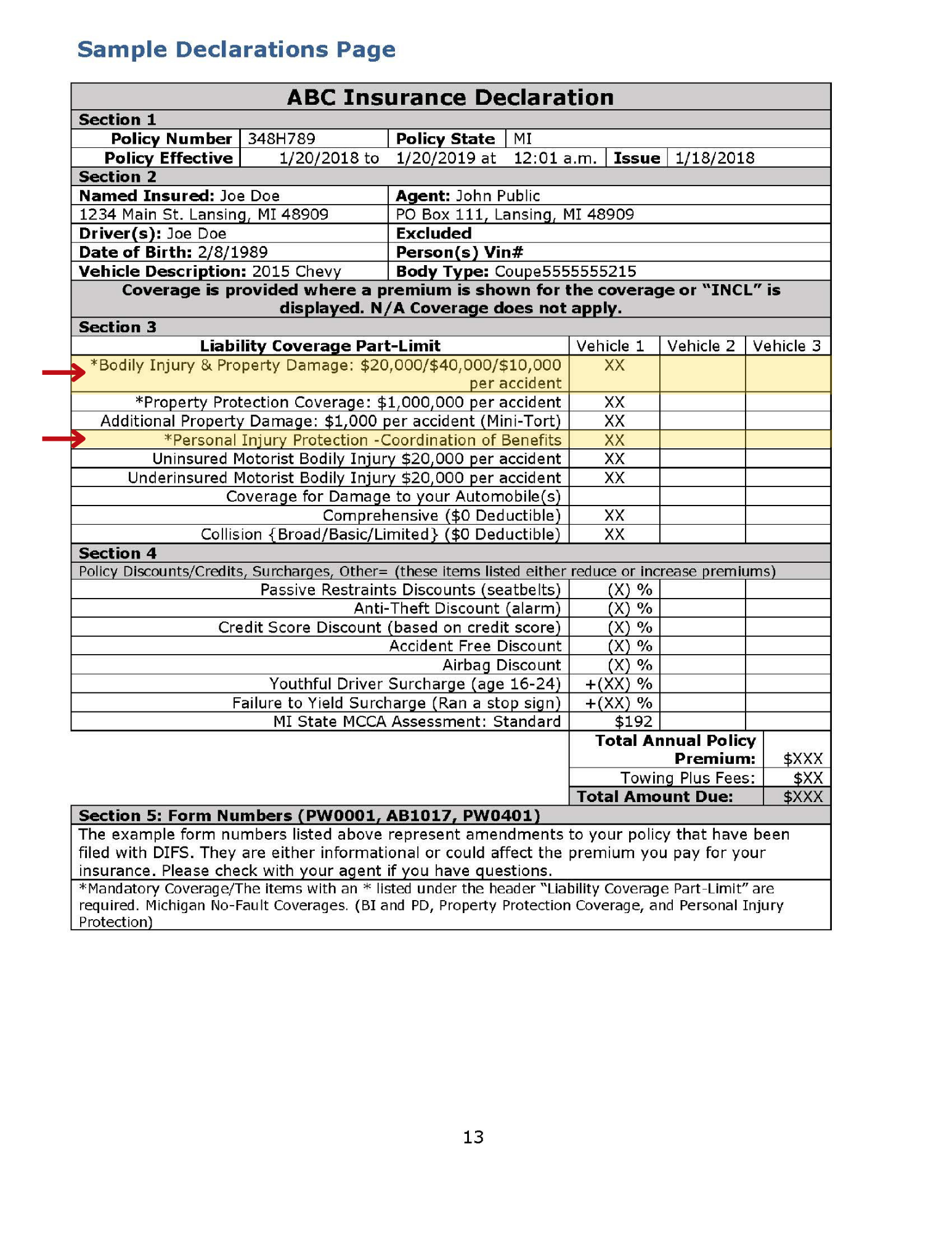

When’s the last time you looked at your car insurance policy? Could you explain what each coverage item means?

If your answer is, it’s been awhile, or please don’t quiz me, you’re in good company. Car insurance is one of the most complex products you can buy.

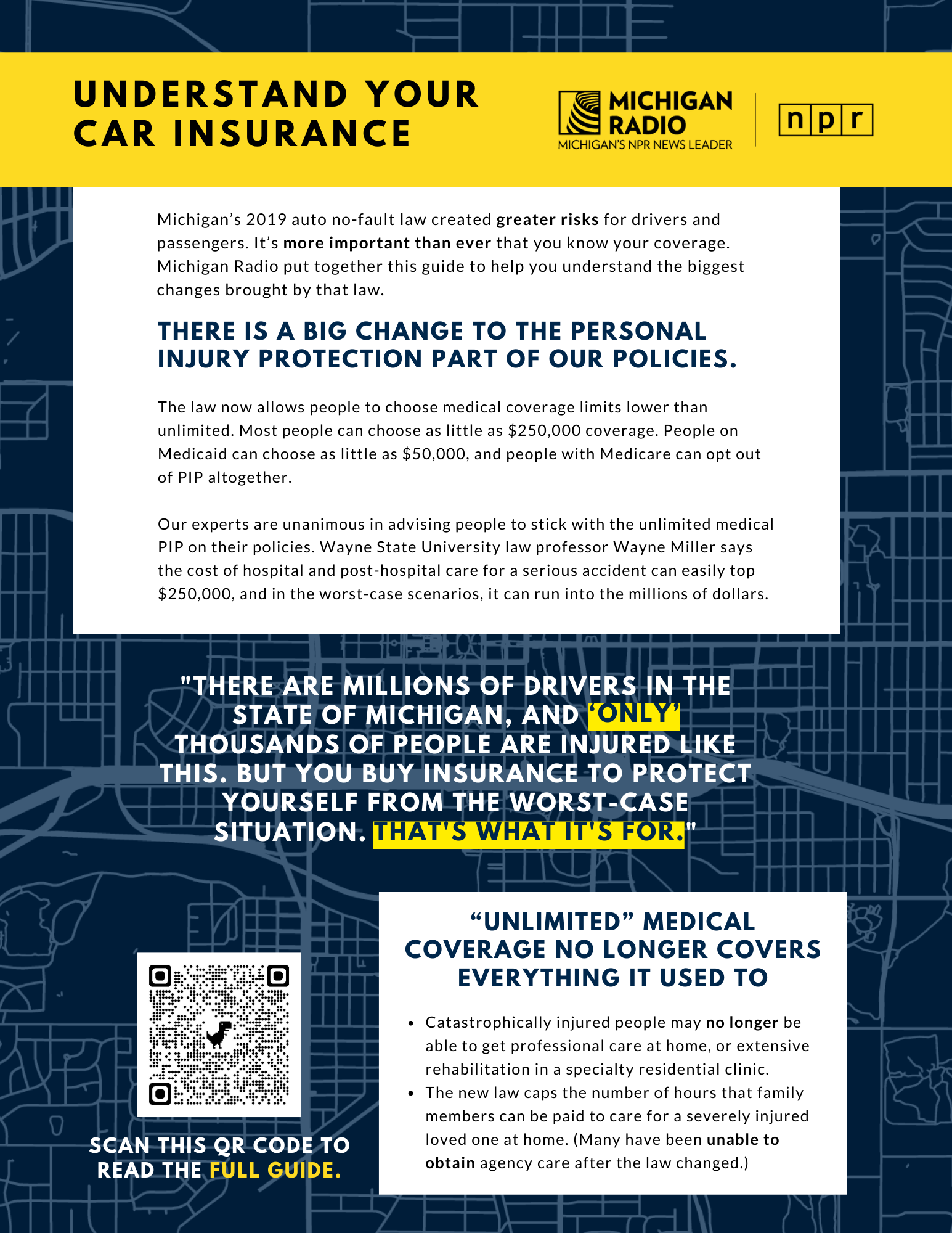

But it’s more important than ever that you understand your coverage. Michigan’s 2019 auto no-fault law created greater risks for drivers and passengers.

We put together this guide to help you understand the biggest changes brought by the 2019 law.

A big change to "PIP," the personal injury protection part of our policies

All drivers in Michigan used to have unlimited medical coverage on their policies, to pay for their own or a passenger’s medical care after a car crash. That coverage is under the PIP (personal injury protection) part of your policy. The law now allows people to choose medical coverage limits lower than unlimited. Most people can choose as little as $250,000 coverage. People on Medicaid can choose as little as $50,000, and people with Medicare can opt out of PIP altogether.

However, the experts we consulted are unanimous in advising people to stick with the unlimited medical PIP on their policies. Wayne State University law professor Wayne Miller said the cost of hospital and post-hospital care for a serious accident can easily top $250,000, and in the worst-case scenarios, it can run into the millions of dollars. Miller said skimping on PIP coverage is “the ostrich approach to buying insurance. You know, ‘That'll never happen to me.’ And of course, statistically, it's not likely that a terrible, costly, life-changing accident will happen to you. There are millions of drivers in the state of Michigan, and ‘only’ thousands of people are injured like this. But you buy insurance to protect yourself from the worst-case situation. That’s what it’s for."

But even "unlimited" medical coverage no longer covers everything it used to

Michigan’s old no-fault law used to require car insurance companies to pay a reasonable rate for medically necessary care for injuries from a car crash, including the most catastrophic, life-long injuries. The 2019 auto no-fault law set rate caps for that care. Brain and spinal cord injury rehabilitation centers, and agencies that provide home care, can only charge 55% of what they used to charge for the care of car crash victims. For the overwhelming majority of these agencies, that amount is less than the cost of providing the care. That’s why so many have either gone out of business, or stopped taking auto accident patients.

So, even though our experts still urge people to keep unlimited PIP, it’s not the same coverage it was before. In many cases, catastrophically injured people will no longer be able to get professional care at home, or extensive rehabilitation services in a specialty residential clinic.

Our story on Annabelle Marsh shows the devastating effect this cap can have.

The law also capped the number of hours that family members could be paid to care for a severely injured loved one at home. Families are limited to a total of 56 hours a week, and have to seek agency care for the rest, if their loved one needs 24/7 care. Many have been unable to obtain agency care after the law changed.

There are new risks, including the risk of being sued

Here’s another “worst-case” scenario that our experts say people — especially people with significant assets — should consider: What happens if you don’t have enough bodily injury liability coverage? That’s the part of your policy that pays for injuries you cause to someone in a crash. Lansing personal injury attorney Steve Sinas said when everyone had unlimited medical coverage, they usually didn’t need to sue the other driver in order to get the care they needed. Now, if they’re injured by someone with significant assets, they are much more likely to sue that person.

“Let’s say a child is playing in the street and you're driving home, and you happen to be wealthy and you look down at your cell phone because you get a text message or something like that, and you fail to see that child and you catastrophically injure that child and they need care for the rest of their life,” Sinas said. “And let’s say their parents bought the $50,000 medical expense coverage because they're on Medicaid, or the $250,000 limit. That kid is only going to be covered up to those limits. So they now have to sue for their medical expenses. Because of that, we now have to insure ourselves more on the other side of the equation, which is with more liability insurance.”

Sinas said affluent people should consider buying “umbrella” policies. An umbrella policy provides extra money, sometimes several million dollars, to cover medical costs for someone you injure, on top of the coverage from your car insurance policy.

He also said that no matter what your economic position, if you can, you should carry uninsured/underinsured coverage. It’s not required by law that you have it, but it adds to the benefits you can claim if you are injured by someone who is driving without insurance, or driving with very low limits.

The new law was supposed to lower the cost of car insurance. Did it?

The short answer is, on average, no. Four years after the no-fault law’s passage, Michigan is once again the most expensive state in the nation for car insurance, according to the consumer website, ValuePenguin.

Doug Heller, director of insurance for the Consumer Federation of America, said the law offered phantom savings, by requiring insurance companies to reduce the cost for personal injury protection, but not other parts of your policy.

“So that savings has been largely eaten up by a shift of the PIP premium to other coverages,” Heller said. ”Insurance companies are free to increase other parts of your premium, and one place where you see that is bodily injury liability. So it's coming out of a different pocket but it's the same pair of pants.”

Click on the images to make bigger.

|

|

On July 1, 2023, your insurance company is required to add a fee of $48 to the Michigan Catastrophic Claims Association assessment on your policy. Even if you don't have unlimited lifetime medical coverage on your policy, which is what the MCCA covers, you will have to pay this extra fee. You can learn more about this fee here.

Doug Heller said if Michigan legislators actually want to lower car insurance costs, as well as make them more fair, they would need to give the Department of Insurance and Financial Services the authority to control insurance company profits, in the same way the Michigan Public Service Commission controls utility company profits. And he said the state would have to limit insurance companies' ability to charge people more based on non-driving factors, such as where they live, or if they don't have an excellent credit score.

What's the best way to lower my car insurance cost?

Wayne State professor Wayne Miller said rather than lower your coverage limits, make a few calls to other insurance companies and see what they would charge you for the same coverage you have now.

“The number one suggestion that I would make is to shop,” said Miller. ”It is truly remarkable the difference between and among insurance companies for the exact same coverage, for the exact same demographic group.”

It’s also good to keep in mind that while you may feel loyal to your insurance company, your insurance company may not feel the same way about you when it comes to setting your rates.

Doug Heller said it’s not an uncommon practice for insurance companies to track your overall purchasing behavior for “loyalty” markers, and charge you more because you tend to stick with the same companies year after year, instead of shopping around.

Wayne Miller said the second-best way to save money on car insurance is to consider dropping collision and comprehensive coverage if your car is more than five years old and you have a safe driving record.

“No matter how well you maintain your vehicle, it's a depreciating asset,” said Miller. “And the insurance cost for it doesn't depreciate very much. So if you really want to save money, consider on older vehicles canceling your collision and comprehensive.”

Finally, you can call your health insurance company and see if you can designate your health insurance as first in line to pay accident costs. This can sometimes lower your car insurance costs a little — but be sure to check with your health insurance company before making any changes to your car insurance policy.

For an explanation of other parts of your insurance policy, check out the state’s guide to coverage here.